|

|

|

|

Teleconsult One stop consultancy |

||||

|

Project Flash Report DPR Collaborations Marketing Finance Opportunities Gifts and Crafts |

Succession Planning Business is a continuous process of capturing opportunities in a dynamic global market where each opportunity is a project. Project is a dream of an entrepreneur. Dream achieved is a history and in dynamic global competition this history always needs to be changed to present reality.

nWho

need Succession Planning?

a. those who want their business to develop and grow with as well

as without them.

b. those who want their family to be happy and economically

independent with as well

as without them.

n

Why succession planning is required?

a. dependency in old age

b.

family responsibilities increase with age

c.

business need continuity or sale

d.

visualization helps you work and plan better

nHow

can we help?

We

can objectively analyze your individual, family and business needs in

the context

of your present and future plan and circumstances which has

significant impact on it.

About Earnings.

a. it is not

linear with age as it was in past. You may get increment or loose

a job or you may get salary reduction instead of increase or you

may get VRS etc.

b.

Employment or business earnings are decided by market. As in business

we have

product life cycles so in job we have life cycle, both equally

vulnerable to competition.

n

c. Increasing

downsizing in companies is a trend not an exception.

n

d. Jobs

have shifted from permanent to temporary, part time, freelance,

franchisee, home based, contractual etc.

e. nBusiness

earnings and salaries are getting internationally stabilized

due to opening up of economies, outsourcing etc.

f. nTax

is unavoidable while planning earnings.

About Family Obligations.

a. nIt

is mostly linear and increases with age. Regular household

expenses are linear.

b. nAfter

household expenses house purchase, children’s/

dependent’s

education/marriages/ dowry, parents medical expenses etc. are

major heads.

n

c. Obligations

are mostly rigid and increase with age.

n

d. If

not well planned it becomes cause of great tension as you grow

old.Other risks mentioned in earnings adds to it.

n

e. Increasing

life expectancy (retired life is more than working life) day by

day is compelling us to provide more for old age expenses.

n

f. Inflation

is reality (salary increments are not) and eats your yield on

investment besides increasing your family obligations.

About Investments.

n

a. Investments

increase with age till marriage then decreases with family

responsibilities.

n

b. Inheritance/

increase of investment many times accompany extra family

responsibilities.

n

c. Risk

may wipe out your investment. It needs to be balanced. Reduce your

risk as you grow old.

n

d. Non-liquid

investment like residential flat, gold etc. may not help you to

plan for old age.

n

e. Investment

in education may reward next generation but will still be an

expenditure for you.

n

f. Increasing

job/business uncertainties can wipe out your investment.

About Business.

n

a. Only

about one out of ten family businesses survives to the third

generation. This only proves the importance of succession planning

beyond doubt.

n

b. If

succession planning is not planned you loose much more in

distressed sale of business/properties than fees of succession

planning professional.

c. nEmotions

with business created by you should not itself become barrier to

it’s

succession.

d. nLack

of succession plan will de-motivate your employees and you will

loose much more in business or it’s

sale.

e. nYour

business may not be worth what you are imagining. Your kids may

have better job avenues than participating in your business.

f. nYou

need to ensure smooth transition for the next generation to take

over the business.

About Career Transition.

n

a. Business

to job or job to business needs succession plan to have smooth

transition.

b. nIncreasing

VRS employees has challenges of facing unfulfilled family

obligations, unwillingness or age barrier to seek fresh job, yet

equipped with enthusiasm & experience to pursue career in

business/ freelance, franchise, part time etc., lack of skill to

identify business opportunities etc.

c. nEven

a job change from one country to another needs a succession

plan especially coming back to home country from overseas jobs.

d. nUnlike

job, business has gestation period.

About migrating to other countries.

n

a. Cost

of living substantially changes and need a lot of homework.

n

b. Earning

potential from job or investments need to be reviewed keeping tax

issues in mind.

c. nSettlement

in new country like house purchase, relocation expenses etc. needs

to be provided adequately.

d. nFamily

responsibilities like education, marriages, parent’s

old age expenses, retirement provision need a close attention.

e. nEmotional

issues of other family members have significant impact on such

decisions and need orientation before taking decision.

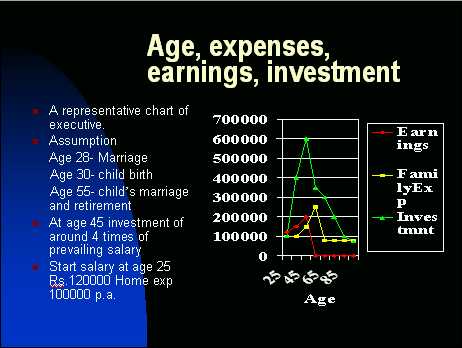

Indicative Age, Expenses and Earnings. Calculate Your Saving

Age, Expenses, Earnings more details.

a. nAt

around 26 you buy house and loan cutting includes in your expenses, at

28 you marry, at 45 age your child starts college education (increase

in family exp), at around 55 age you plan to marry your child (exp for

family responsibility) and you retire.

b. nHome

expenses remain linear and does not come down almost even after 55 age

when the child become financially independent as your medical expenses

increase.

c. nYou

consume your investment for marriages and other family

responsibilities.

d. nYour

retirement life many times is more than your working life.

e. nPresent

interest rate around 4% are lower than inflation around 5%.

Remember.

n

a. Do

not postpone succession plan.

b. nLesser

investment needs more guidance of succession planning professional as

your investment is much more precious to you.

c. nAvoidance

or postponement of consultation will only invite complex problems in

future.

d. nConsult

proper and independent professional who does not give you any other

professional service than succession planning as he will not have

vested interest in you for other fees. Don't go for cheap consultancy,

you will get the same results.

e. nIdentify

your successor in business.

f. nKeep

open mind to discuss all angles of succession plan with succession

planning professional.

g. nSuccession

planning professional will guide you even to take assistance of your

existing professionals.

n

h. Like

we teach our child to walk we need to do the same for

business/ family succession. i. It

is not only money but also visions, dreams and emotions.

j. nIt

is helping you objectively to manage people around you and

resources with you to suite the best for your unique situation

from both economical and emotional point of view.

k. nNothing

will survive longer than the vision, dreams and thoughts which you

have shared with people around you, we only help your team to

translate it in reality and pass it on further.

Case 1 What if?

nMr.

Ajay age 42 a senior executive in India drawing 6 lac p.a. suddenly

realizes that his company is not doing well and it is right time to

exit. He has invested 12 lac in residential flat and has 8 lac liquid

investment. He got next offer with 4 Lac. This year his 18 year

daughter want to join a city college costing him around Rs. 2.5 lac

p.a. His younger son is in SSC and will be going to college after 2

years. He has no pension.

a. What if he gets job after 6 months/ 1 year?

b.

What if his parents medical expenses increases as they will be around

70 years old?

c.

What will he do for daughter’s

marriage after 4 yrs?

d.

What if his son gets admission in USA for BS?

Case 2 What if?

nMr.

Kapoor age 43 executive in gulf saving 15 lac p.a. , investment

75 lac migrates to Canada, his living cost there is 30,000 USD

p.a or 13.5 lac p.a., he estimated that he will get job of 4000 usd

p.m. within 2/3 months but is still looking for job after 6 months.

Wife understands the situation but children are happy in school and

surroundings. Daughter will go to college this year and education will

cost further by 12000 USD p.a.

a. Should he come back to Gulf/ India? If so how will he handle

emotional issues of children?

b. Should he continue in Canada searching his job till he

exhaust his saving?

c. if (a) does he know prevailing living cost in localities

where he has his flat, available job opportunities,

educational expenses, willingness of his and family to get absorbed in

Indian fast, hectic life? Will his 2nd job

offer in gulf be same?

Case 3 What if?

nMr.

Chaudhary an Indian entrepreneur age 48 earnings around 6 lac p.a. has

grocery shop. He has investment of 25 lacs son age 22 (finished

college), daughter age 20, both parents are staying with him,

son/daughter are intelligent and have good academic credentials. He

wants to marry daughter in this year and marriage will cost around 5

lac. He has his ancestral home and is happy with present position. Now

he wants his son to take over his business but son feels that his job

offer of 6 lac at present without any headache is worth more than 6

lac annual earnings from business. Mr chaudhary devotes minimum 12

hours for his business every day many times even Sunday is not spared.

Since last 5 years they have not gone on family picnic.

a.

Should he sell/ give franchise/ give on profit sharing his business

built over 30 years? If so what will be the financial implications?

b. After 7 years he may have investment of approx 28 lac his living

exp are around 180,000 and interest will be around 84,000 at 3% What

should he do?

c. He noticed that upcoming neighboring malls will erode his earnings

and potential sale value of his business too, but does not know

whether to postpone or not the sale of his business.

Thoughts worth pondering.

a. nNothing

but change is permanent. When you are busy creating your wealth

you may be unaware of the changes around you or in your home

country or in a country where you plan to migrate. Each time is

right time to plan for succession.

b. Postponement

of problem will always create more problem as expenses are linear

but not the earnings, family responsibilities are directly

proportional to age, investment once wiped out is almost

impossible to rebuild after retirement.

c. A stitch in time will always save nine. If you cannot improve

at least you can prevent it from worsening.

d. When compelled by circumstances you always loose your buying

power whether in business or job.

e. As you share your joys and happiness with family share your

concerns too. Nowhere in the world you have stronger family system

than India where parents are treated as God & home a temple.

Children get an overview of generations from grandparents in a

very friendly way which no professional or school can teach.

f. Let your visions, dreams and emotions flow continuously to be

shared by all family members, it will last more than your money.

g. In today’s world nuclear families and working women are

common and have wider challenges to play multiple roles.

h. Everything that you earn may not always be under your

control, sometimes for small efforts you may get big and

sometimes nothing at all in spite of long efforts. But in

general easy come easy go.

n

i. Change

is permanent and change always results from actions. It is great

skill in life to bear the things you cannot change and to

empower our actions to work on the things we can change.

n

j. As

you discard your clothes so does the atma discards body is said

in Gita. We too need to have open mind to discard old

unsustainable thoughts in today’s

changing world to give birth to new rejuvenated ideas ready for

tomorrow’s

world carrying the same indestructible atma but in different

clothes.

Family Businesses.

a. nTen years after India opened up its economy to multinationals and global competition, the country's family-run industrial empires remain intact and stronger than ever.

b. nThe

aggressive Ambani brothers Mukesh, 44, and Anil, 42, sons of the

firm's 68-year-old founder Dhirubhai Ambani, call the shots at

Reliance, while the more reticent Kumarmangalam Birla,34 takes all

major decisions at the $6.4-billion Birla group which spans metals

and insurance

c. nLiberalization

has encouraged people to start their own firms, and there is a

resurgence in family-run businesses as a whole.

d. nThere

were 80,000 company start ups in 1998-99, and these firms will see

maximum growth in the first 20 years of their life.

e. nFamily-run

businesses have advantages: risk-taking ability, speed of decision

and long-term vision," says Manesh Shrikant, dean of Bombay's

S P Jain Institute of Management & Research.

f. nBut

increased competition has seen a shakeout of some well-known

names. “

A large number of family-run companies have failed," says

Shrikant. "And families have too often enriched

themselves at the cost of companies they have founded."

n

g. Often

family-run companies have been bound by tradition and not

moved fast enough."The Mafatlals (chemicals), Sarabhais

(pharmaceuticals), Walchand (engineering), Modis (rubber) have

fallen behind as they have not kept up with the times,"

says Gita Piramal, author of the much-acclaimed Business

Maharajas, a book on Indian business families.l

n

h. Cases

where families have handed operations over management to

professionals are the exception rather than the rule in India

like Thermax, Ranbaxy Laboratories.

n

i. The

Marwaris, who controlled Indian business for a half century

are falling away fast, while entrepreneurs have sprung up in

all communities," says Gita Piramal.

Education and saving for future generations is a priority.

a. nReferring

to the investment profile of the South Asian community, Chopra said:

"Studies by Merrill Lynch have shown that South Asians are highly

conservative with a very strong propensity towards saving. Education

and saving for future generations' educational needs continues to be a

top priority.

b. n"Retirement

saving and financial planning is also extremely important,

particularly among South Asian physicians and healthcare providers. We

have found from a business standpoint considerable success in the

following sectors: technology entrepreneurs, physicians and health

care providers, small business owners and corporate executives. And

most of the wealth we are finding has been sourced largely through

work or work related accomplishments.“

Real saving potential starts after 40s.

The

higher your salary, usually the higher your discretionary savings ratio.

Before the age of 40 it is difficult for most salary earners to

accumulate significant savings. Usually expenses on children, the house,

and transport are too high to make meaningful savings possible.

Accordingly at the start of your working life your savings as a

percentage of after tax income will often be around 5% (slightly less

for lower-skilled workers and slightly more for management). However,

after the age of 40 your discretionary savings ratio should rise

steeply, say, to some 10% for unskilled workers and to about 30% for

chief executives. Over your entire working life, savings should ideally

average not less than 10% of after-tax income and for executive

management an average savings ratio in excess of 30% is strongly

recommended.

How can you afford to ignore your succession plan? Contact us and explore your options. Home |